[ad_1]

Here’s a thought for investors: If the Federal Reserve raises interest rates to 5% or more would that wreck the economy and stock prices ?

The U.S. stock market has been rallying to start 2023, clawing back a big chunk of the painful losses from a year ago. The bullish tone has been linked to a view that the Federal Reserve will need to cut interest rates this year to prevent a recession, reversing one of its quickest rate-increasing campaigns in history.

Doomsday investors, including hedge-fund billionaire Paul Singer, have been warning against that outcome. Singer thinks a credit crunch and deep recession may be necessary to purge dangerous levels of froth in markets after an era of near-zero interest rates.

Another scenario might be that little changes: Credit markets could tolerate interest rates that prevailed before 2008. The Fed’s policy rate could increase a bit from its current 4.75%-5% range, and stay there for a while.

“A 5% interest rate is not going to break the market,” said Ben Snider, managing director, and U.S. portfolio strategist at Goldman Sachs Asset Management, in a phone interview with MarketWatch.

Snider pointed to many highly rated companies which, like the majority of U.S. homeowners, refinanced old debt during the pandemic, cutting their borrowing costs to near record lows. “They are continuing to enjoy the low rate environment,” he said.

“Our view is, yes, the Fed can hold rates here,” Snider said. “The economy can continue to grow.”

Profits margins in focus

The Fed and other global central banks have been dramatically increasing interest rates in the aftermath of the pandemic to fight inflation caused by supply chain disruptions, worker shortages and government spending policies.

Fed Governor Christopher Waller on Friday warned that interest rates might need to increase even more than markets currently anticipate to restrain the rise in the cost of living, reflected recently in the March consumer-price index at a 5% yearly rate, down to the central bank’s 2% annual target.

The sudden rise in interest rates led to bruising losses in stock and bond portfolios in 2022. Higher rates also played a role in last month’s collapse of Silicon Valley Bank after it sold “safe,” but rate-sensitive securities at a steep loss. That sparked concerns about risks in the U.S. banking system and fears of a potential credit crunch.

“Rates are certainly higher than they were a year ago, and higher than the last decade,” said David Del Vecchio, co-head of PGIM Fixed Income’s U.S. investment grade corporate bond team. “But if you look over longer periods of time, they are not that high.”

When investors buy corporate bonds they tend to focus on what could go wrong to prevent a full return of their investment, plus interest. To that end, Del Vecchio’s team sees corporate borrowing costs staying higher for longer, inflation remaining above target, but also hopeful signs that many highly rated companies would be starting off from a strong position if a recession still unfolds in the near future.

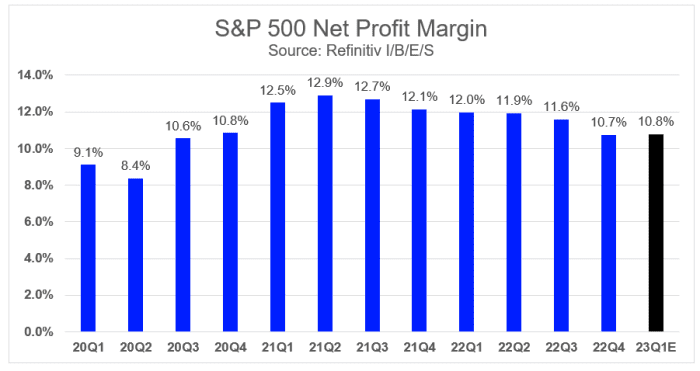

“Profit margins have been coming down (see chart), but they are coming off peak levels,” Del Vecchio said. “So they are still very, very strong and trending lower. Probably that continues to trend lower this quarter.”

Net profit margins for the S&P 500 are coming down, but off peak levels

Refinitiv, I/B/E/S

Rolling with it, including at banks

It isn’t hard to come up with reasons why stocks could still tank in 2023, painful layoffs might emerge, or trouble with a wall of maturing commercial real estate debt could throw the economy into a tailspin.

Snider’s team at Goldman Sachs Asset Management expects the S&P 500 index

SPX,

to end the year around 4,000, or roughly flat to it’s closing level on Friday of 4,137. “I wouldn’t call it bullish,” he said. “But it isn’t nearly as bad as many investors expect.”

“Some highly levered companies that have debt maturities in the near future will struggle and may even struggle to keep the lights on,” said Austin Graff, chief investment officer at Opal Capital.

Still, the economy isn’t likely to “enter a recession with a bang,” he said. “It will likely be a slow slide into a recession as companies tighten their belts and reduce spending, which will have a ripple effect across the economy.”

However, Graff also sees the benefit of higher rates at big banks that have better managed interest rate risks in their securities holdings. “Banks can be very profitable in the current rate environment,” he said, pointing to large banks that typically offer 0.25%-1% on customer deposits, but now can lend out money at rates around 4%-5% and higher.

“The spread the banks are earning in the current interest rate market is staggering,” he said, highlighting JP Morgan Chase & Co.

JPM,

providing guidance that included an estimated $81 billion net interest income for this year, up about $7 billion from last year.

Del Vecchio at PGIM said his team is still anticipating a relatively short and shallow recession, if one unfolds at all. “You can have a situation where it’s not a synchronized recession,” he said, adding that a downturn can “roll through” different parts of the economy instead of everywhere at once.

The U.S. housing market saw a sharp slowdown in the past year as mortgage rates jumped, but lately has been flashing positive signs while “travel, lodging and leisure all are still doing well,” he said.

U.S. stocks closed lower Friday, but booked a string of weekly gains. The S&P 500 index gained 0.8% over the past five days, the Dow Jones Industrial Average

DJIA,

advanced 1.2% and the Nasdaq Composite Index

COMP,

closed up 0.3% for the week, according to FactSet.

Investors will hear from more Fed speakers next week ahead of the central bank’s next policy meeting in early May. U.S. economic data releases will include housing-related data on Monday, Tuesday and Thursday, while the Fed’s Beige Book is due Wednesday.

[ad_2]

Source link

Leave a Reply